Can a Disabled Vet Have Private Health Insurance

4 August 2017

PDF version [397KB]

Amanda Biggs

Social Policy Department

Introduction

The financing arrangements for health care in Australia are complex, reflecting both historical developments unique to Australia and its federal system of government.

Australia's health organization is a mix of public and private wellness care. Broadly, publicly-financed wellness intendance primarily refers to services funded through government programs such as Medicare and the Pharmaceutical Benefits Scheme, also every bit public hospital services that are jointly funded by the Commonwealth and us and territories. In addition, some health services are funded through private health insurance, individual out-of-pocket payments, and 3rd party insurers such equally motor vehicle insurers.

Information technology is not mandatory to take individual health insurance embrace. Nether Medicare, all Australians are eligible for subsidised medical treatment and free treatment as a public patient in a public hospital. However, private health insurance provides a selection of doctor, can help with the cost of treatment in a private hospital, and the toll of ancillary treatments not covered by Medicare such equally dental, optical and physiotherapy.

This quick guide outlines the broad arrangements around individual health insurance that exist today. Information technology provides brief information on the industry and regulatory arrangements, private health insurance membership and types of cover, regime surcharges and incentives, and primal features of private health insurance in Australia.

Electric current private health insurance arrangements

Individual health insurance sector

The origins of private wellness insurance lie in the friendly and mutual societies that developed in the 19th century, which, for a contributory fee, provided members with a range of medical services. These entities were typically linked to a specific industrial sector, such as railway workers, police or teachers.

Today'south private health insurance sector comprises some 37 registered individual health insurers, a mix of not-for-profit insurers (mutual organisations) and for-turn a profit insurers. This number as well includes restricted membership funds which only provide embrace to members of a specified industry or group. Private wellness insurers must comply with regulatory and prudential standards, including those listed below. Individual health insurers can operate nationally, or be based in a particular jurisdiction or region.

Co-ordinate to industry regulator APRA, in 2015–16 private wellness insurers paid nearly $nineteen billion in benefits to members (run across tab 'Fin Perf'). Of this $fourteen billion in benefits was paid for hospital handling which includes handling in private hospitals, public hospitals, solar day hospitals and hospital substitute treatment (run into tab 'Bens by Cat'). Revenue (primarily from premiums, simply besides from investments) totalled effectually $22.5 billion. Management expenses totalled effectually $ane.nine billion, or 8.5 per cent of total revenue (meet tab 'Fin Perf').

Legislation and governance

Private health insurance is regulated primarily nether the Private Health Insurance Act 2007 , the Individual Health Insurance (Prudential Supervision) Act 2015, and related rules and regulations. Private wellness insurance is administered past the Department of Health with prudential oversight provided by the Australian Prudential Regulation Authority (APRA), a role previously performed by the Private Wellness Insurance Administration Council. Consumer complaints are handled by the Private Health Insurance Ombudsman, which sits inside the Office of the Commonwealth Ombudsman and produces a Land of the Health Funds report annually. Broader consumer and competition issues are dealt with by the Australian Consumer and Competition Commission (ACCC), which likewise provides almanac reports on the sector to the Senate.

Types of private health insurance

In that location are two types of private health insurance: hospital, and general treatment (sometimes called coincident or extras)—or these tin exist combined. Private health insurance does not cover services that are provided out of hospital and which are covered past Medicare, such as general practitioner services. Private health insurance coverage for the cost of ambulance services varies across jurisdictions. Private wellness insurance is available for singles, couples, and families.

Private hospital cover

Private hospital insurance only covers services for which a Medicare do good is payable, as listed in the Medical Benefits Schedule (MBS). Services not listed in the MBS, such as plastic surgery for corrective reasons, are non covered by private health insurance. Hospital encompass includes hospital substitute handling, such every bit hospital-in-the-dwelling care (subject to medical blessing).

Medicare covers 75 per cent of the listed Medicare fee for hospital services; private hospital insurance covers the remaining 25 per cent (known as 'the gap'). Private hospital insurance may encompass part or all of whatsoever amount charged above the gap, and some or all of the costs of accommodation and operating theatre fees, drugs, prostheses, and diagnostic tests, depending on the policy and whether the insurer has agreements with hospitals.

Broadly, four levels of private hospital encompass are offered, with varying levels of exclusions or restrictions:

- public comprehend—covers the lowest do good permitted in a public infirmary, but the patient retains a choice of doctor

- basic comprehend—low level benefit roofing a minimal number of services with a range of exclusions and out-of-pocket costs

- medium cover—includes some restrictions and exclusions, but covers a broader range than basic cover and offers lower benefits than superlative cover and

- top cover—comprehensive; must cover all services listed in the MBS.

The National Health Reform Agreement allows patients with private infirmary insurance who are admitted to a public hospital to choose whether to exist admitted as a public or private patient. A recent report from the Contained Hospital Pricing Dominance shows that the proportion of public hospital activity funded through private health insurance has grown in recent years and suggests this is driven past public hospitals encouraging patients to employ their individual cover. This has prompted the Australian Private Hospitals Association to express concern that this may bulldoze up the price of private health insurance premiums, while the Health Minister Greg Hunt said he would exist concerned if this lengthened public hospital waiting lists.

General or ancillary cover

General handling (or ancillary or extras embrace) provides benefits for out-of-hospital services such every bit dental, optical, physiotherapy, natural therapies and non-Pharmaceutical Benefits Scheme medicines.

Membership levels

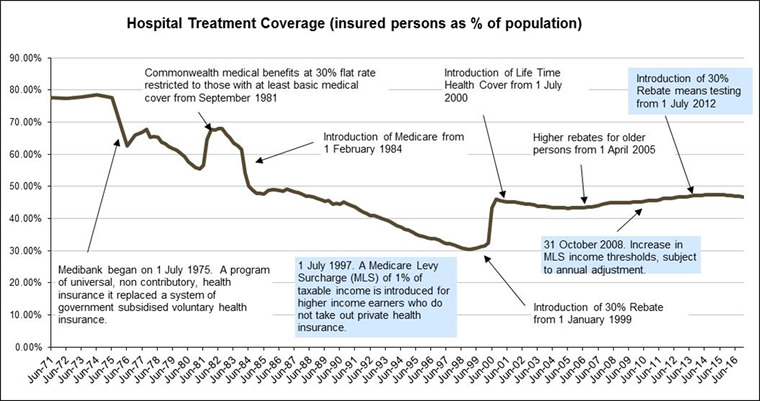

According to APRA statistics, equally at March 2022 some 11.iv million Australians had private infirmary cover (around 46.v per cent of the population) and 13.5 million had ancillary or full general cover (around 55.five per cent of the population).

Private health insurance membership as a proportion of population initially savage after Medicare was introduced in 1984 (come across nautical chart below from APRA). However, following the introduction of measures to encourage membership, the proportion covered increased. Since September 2015, private hospital coverage every bit a proportion of the population has declined from 47.4 per cent to 46.5 per cent.

Hospital treatment coverage (insured persons equally a proportion of population)

Source: APRA

Complexity of products

Private health insurance is becoming more complex. A range of dissimilar co-payments, exclusions and restrictions can apply, making it increasingly difficult for consumers to cull a suitable policy. The number of insurance products on offer is not clear either. In the ACCC's 2014–15 report to the Senate, it estimated there were around 46,500 private wellness insurance products as at June 2022 (p. 35). More recently, the Private Wellness Insurance Ombudsman clarified that this estimate (based on the number of Standard Information Statements (SIS) which summarise the key product features) included products that are no longer available. Removing these brings the total number of SISs to 27,281 equally at January 2017, but this also includes products offered by restricted membership funds.

The authorities advises consumers to store around for the best value. Consumers can apply a authorities website to compare policies, or they can use a number of commercial comparator websites. Notwithstanding, according to a recent Choice survey, consumers yet report difficulties in comparing policies.

Consumer incentives and penalties

As already noted, a number of government incentives and penalties apply to encourage greater participation in private health insurance. These are explained briefly below.

Lifetime Wellness Embrace

Introduced by the Howard Government in July 2000, Lifetime Health Comprehend (LHC) is a 2 per cent almanac loading on the toll of premiums for people over 31 who delay taking out private health insurance. The maximum loading is 70 per cent. It means that a person who takes out hospital cover at historic period twoscore for the first fourth dimension will pay xx per cent more on their premium than someone who buys the same infirmary comprehend at age 30. After ten years of continuous cover any LHC will terminate to apply. Those with LHC are allowed specified 'permitted days' without cover. For example, if they travel overseas they tin can cull to exist without hospital cover for periods totalling i,094 days (or three years).

According to the latest industry statistics, in March 2022 some xiii per cent of adult policyholders had incurred a LHC loading.

Individual wellness insurance rebate

The private wellness insurance rebate is an income-tested government rebate on the cost of private health insurance premiums for hospital, general treatment and ambulance policies. Introduced in 1999, the rebate originally provided a thirty per cent disbelieve on premiums for those under 65, with college rebates for older Australians. Income testing was introduced in 2012, resulting in those on incomes above an indexed threshold receiving a lower rebate or no rebate at all. From 2014, the calculation of the rebate changed from a flat 30 per cent (college for older policyholders) to the deviation betwixt the Consumer Toll Index (CPI) and the manufacture weighted average increment in premiums. Over fourth dimension, this has resulted in a lower rebate being available. Income tiers and their applicable rebate levels are published by the Regime each year from 1 April. The income tiers used for income testing are normally indexed annually, only were frozen at 2014–xv levels until 2022 every bit role of a Upkeep Savings Measure out. The Government appear in the 2016–17 Budget that it would maintain the freeze until 2021. Legislation to enact this extension was passed in September 2016.

Medicare Levy Surcharge

The Medicare Levy Surcharge (MLS) is an additional levy (on peak of the two.0 per cent Medicare levy) imposed on high-income earners who decline to buy private health insurance. The surcharge is calculated at a rate of between ane.0 to 1.5 per cent of income.

The same budget savings measure which froze the income tiers for the private health insurance rebate has also frozen the income tiers for the purpose of determining liability for the MLS.

Features of individual wellness insurance in Australia

Private health insurance in Commonwealth of australia has some notable legislated features.

Customs rating

Private health insurance in Australia is community rated, not adventure rated like other insurance products such every bit life insurance. Customs rating requires that private wellness insurance policies exist offered at the same cost irrespective of an private'due south risk factors such equally age (autonomously from the LHC age loading), health condition, previous claiming history or how ofttimes they need health care. Individual wellness insurers participate in a risk equalisation scheme which partially compensates insurers with a riskier membership profile.

Portability and waiting times

The portability dominion allows consumers to switch to some other policy with a different insurer without incurring additional waiting times, provided the new policy offers the same level of benefits equally their old policy. Certain limits and restrictions use. Individual wellness insurers can impose a 12-month waiting period before hospital benefits tin be claimed by a newly joined member or someone upgrading to more expensive cover if the person has signs or symptoms of a pre-existing condition. A 12-month waiting period for obstetrics, and a two calendar month waiting flow for psychiatric care, rehabilitation, palliative care and other services on new or upgrading members tin can also be applied.

If a person has already served out office of a waiting flow on their previous policy, the balance of the waiting period will utilize on the new policy, provided there are no added benefits or ameliorate weather condition nether the new policy.

Broader Wellness Cover

Individual wellness insurers can besides offer coverage for hospital substitute handling (such equally infirmary-in-the-domicile) and programs to aid manage chronic diseases, under Broader Health Encompass arrangements.

Private health insurance reforms

The Individual Health Ministerial Advisory Committee was established in September 2022 to advise the Minister for Wellness on a range of reform options. Its Terms of Reference include developing simpler categories of insurance (such as gold, silverish, bronze), empowering consumer choice, transparency and affordability improvements, improving value for rural and regional consumers, culling funding models for full general treatment and other problems every bit directed by the government minister. The Committee was established following a consultation process in 2015–xvi and a consumer survey which revealed a number of consumer concerns with private wellness insurance.

Separately, the Senate Community Diplomacy Legislation Committee is undertaking an research into the value and affordability of private wellness insurance and out-of-pocket medical costs.

For copyright reasons some linked items are only available to members of Parliament.

© Commonwealth of Commonwealth of australia

![]()

Creative Commons

With the exception of the Commonwealth Coat of Arms, and to the extent that copyright subsists in a third political party, this publication, its logo and front end page design are licensed under a Artistic Commons Attribution-NonCommercial-NoDerivs 3.0 Australia licence.

In essence, you are free to copy and communicate this piece of work in its current grade for all non-commercial purposes, as long as y'all attribute the work to the writer and bide past the other licence terms. The work cannot exist adapted or modified in whatever way. Content from this publication should be attributed in the post-obit way: Writer(due south), Championship of publication, Series Name and No, Publisher, Date.

To the extent that copyright subsists in third party quotes it remains with the original owner and permission may be required to reuse the cloth.

Inquiries regarding the licence and any use of the publication are welcome to webmanager@aph.gov.au.

This work has been prepared to back up the work of the Australian Parliament using information available at the time of product. The views expressed practise not reflect an official position of the Parliamentary Library, nor do they constitute professional legal opinion.

Any concerns or complaints should be directed to the Parliamentary Librarian. Parliamentary Library staff are available to discuss the contents of publications with Senators and Members and their staff. To admission this service, clients may contact the author or the Library's Key Research Point for referral.

Source: https://www.aph.gov.au/About_Parliament/Parliamentary_Departments/Parliamentary_Library/pubs/rp/rp1718/Quick_Guides/PrivateHealthInsurance

Post a Comment for "Can a Disabled Vet Have Private Health Insurance"